Harvesting Global Macro Factors by Creating a Better HF Index Return Profile - Part 2

how to beat the Hedge Fund Industry …

Why?

There are very few macro factors that influence all markets given by the fact that many markets exhibit high correlations during bad times. Independent macro factors and thus risk premia, can be derived, depending on the literature, as those that represent growth, inflation and volatility or risk aversion. This means that the number of true independent bets are relatively low and in a traditional portfolio, this might vary between 1 and 2.

There are long term risk premiums associated with these factors that can be constructed through the use of allocations to equities, nominal bonds and commodities.

One way to do so is the “Risk Parity” portfolio or the allocation of equal risk between equities, fixed income, and commodities.

However, the issue with Risk Parity was that it assumed that each separate asset class was truly orthogonal. However, holding different asset classes in of itself is not necessarily diversification given it’s simply a representation of an exposure to the actual underlying macro drivers of markets.

It couldn’t be the case that the drivers influencing these assets could overlap and reduce the number of independent bets, particularly on the downside.

One study found that a global 60/40 and permanent portfolio (25 stocks / 25 bonds / 25 gold / 25 cash) dominated nearly all risk-parity strategies on multiple time frames:

@Risk Parity Not Performing? Blame The Weather. - MPI

This is not to mention that risk parity is inherently tax inefficient which could result in a roughly 26.8%* return hit, or on average 1.7% annually looking at the 10 year performance (2015-2024) of the S&P 10% Risk Parity Index

A better way to access these long term premiums is through a gross-of-fee exposure to Hedge Funds.

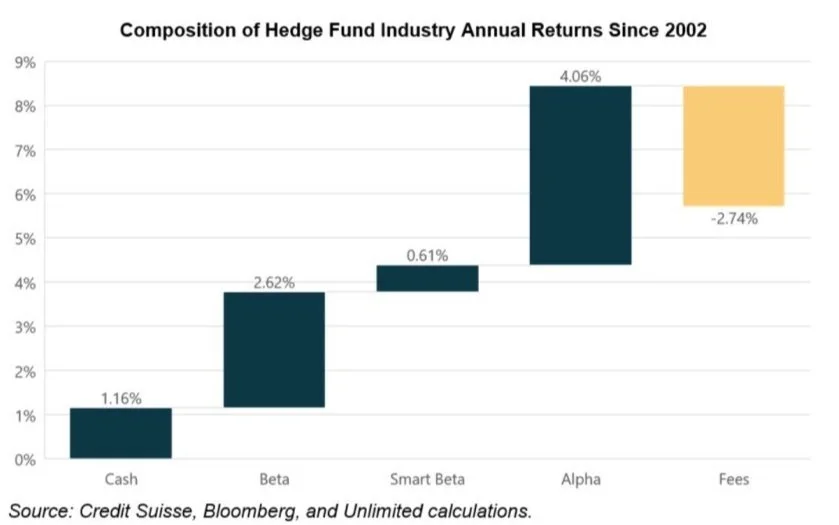

Here is the return attribution of Hedge Funds since 2002:

The way to improve this return attribution is removing the fees altogether and reducing the impact of taxes to as close to 0 as possible which includes the cash attribution. Since Hedge Funds are also tax inefficient vehicles, the alpha could be fully eroded by a further 2-3%, leaving behind very muted upside beta exposure relative to the beta downside risk.

But, why do Hedge Funds (pre-tax gross-of-fee) have Alpha?

Hedge Funds exposure can be obtained through the use of timed exposure to different common factors. In that sense, it’s easy to understand where the alpha comes from.

The alpha is simply derived from putting together different factors and hopefully obtaining more exposure to an underlying market driver that is diversifying to the one driving the benchmark equity beta.

An easy to understand example is that that stocks + bonds have a higher risk adjusted returns than either alone. But that’s not all because Hedge Funds opportunistically weigh these exposures.

But market timing is impossible…

Yes, but it is not necessarily the overall timing of factor exposures like equities that matter here given that Hedge Funds always have on beta exposure, but the relative weighing of the different macro drivers obtained through an exact allocation towards stocks, bonds, credit, and commodities.

Clearly, that has resulted in outsized (pre-tax gross-of-fee) alpha that represents an attractive source of returns. Aggregate active alpha strategies are thus far significantly more appealing than static systematic single manager ones like risk parity.

This alpha has degraded over time, but does still exist.

The Hedge Fund Paradox

Ok, we’ve established that hedge fund exposure can be obtained, with very little tracking error, through varying exposures to different markets.

But, if this is what Hedge Funds are, why can’t you try and construct your own allocation towards these markets (stocks, bonds, etc…)?

We’ve established that Hedge Fund Indices are consistently top percentile performers (cross-sectional positive skew). Theoretically, any single manager product is destined to underperform on a risk-adjusted basis and will only outperform via a mere small random chance.

The overall relative weighting of these markets represent the collective wisdom of the most sophisticated investors in the world. As Hedge Fund assets, remain a small minority of overall invested assets, this collective view has been demonstrated to be incredibly useful to generating outsized alpha.

In that sense, any other relative weighting of these markets will underperform due to being akin to a single-manager strategy and deviating from the strongest conviction outlook.

But what about Private Equity?

Ok, so it is possible to closely track Hedge Fund styles ex-post. A similar method can also be applied to replicating a Private Equity Index (Cambridge Associates). But is this actually appealing and what does that suggest about this particular asset classes or adjacent ones like Venture Capital?

Unlike Hedge Funds, these asset classes represent a constant leveraged equity exposure but, just like the former, individual fund performance is not persistent and the Index is a consistent top percentile performer.

The ingredients to closing tracking this Index are time varying leveraged sector bets. Does this make for a particularly attractive investment? Unlike Hedge Funds that care about risk adjusted returns, Private Equity is trying to obtain the highest possible gross return by over and under weighing sectors within the economy like small cap, tech or healthcare. However, leverage nulls this point, because why not just leverage market cap weighted equities?

Proponents of market efficiency would argue that market cap weighted equities remain the most efficient risk-adjusted way to obtain equity exposure. We take a different approach and suggest that this implies Private Equity, as an asset class, is actually more akin to a single-manager strategy and that there should be little reason why Private Equity is an efficient use of capital on a risk adjusted basis compared to market cap weighted equities.

Why replication works so well

Here are the return distributions of pre-tax and post-tax performance of an example HF replication:

Bob Elliot - Imperfect Replication Beats Single Manager 9/10 Times @ unlimited

In this particular example, the results are profoundly in favor of the replication, however, taxes still result in a roughly 2% hit per year.

In comparison, in this example, we’re aiming for near passive tax expenditure, utilizing similar techniques as in our managed futures offering. Also, from a replication point of view, Hedge Fund indices are actually an easier endeavor than Managed Futures.

However, we change around some things that we expect will bring significant improvements:

- Tax minimization

- Uncertainty minimization or investor appetite for returns that deviate too far from benchmarks like market cap equities

- Transparent and Intuitive portfolio allocation

- Transaction cost minimization

Our Goal

Simply put: tracking, but aiming to beat a gross Index of diversified Hedge Funds using mostly the same 5-factor universe as our managed futures offering (saving on transaction costs if the two are combined): SP500, Euro, 10-year treasuries, Gold and WTI Crude Oil.

We use a similar underlying engine or our proprietary “triple-layered” replication approach as our managed futures product with a slight twist.

However, as Hedge Funds in general are fairly tax inefficient we also prioritize achieving a very low tax burden so that long term performance can remain in line with our Index, and we achieve that with our propriety approach. Thus, this is our dual mandate.

As we’ve alluded to in previous posts, a HF Index is a consistently top percentile performer in both total and risk adjusted returns. There are variety of Hedge Fund strategies within the Index:

Long/Short Equity and Event-Driven

Fixed Income Arbitrage/Relative Value

Global Macro and Managed Futures

Multi-strategy

Emerging Markets

First, we do replication on each subcategory which is an equal weighted Index of all fund constituents in that category. Then, these are put together to create a final Index where categories have weights according to that categories AUM relative to all other strategies.

Why isn’t there direct exposure to a variety of additional markets?

Since we prioritize low taxes, we utilize our triple-layered engine to map the exposures to a more efficient set of markets. Generally, credit such as domestic and international high yield, investment grade and mortgage-backed securities can be replicated using a mix of market beta, treasury exposure, fx, and commodities to create a tax profile 3-5x more efficient.

Emerging Markets funds are generally tax inefficient as well, however, those funds still provide valuable insights to adjust exposures to our universe of markets like equities and commodities and still generate a return profile much inline with actually having emerging markets exposure.

The Long/Short and Event-Driven equity exposure can be further drilled down by factors like momentum, value and quality or by sectors like tech, healthcare, energy, financials and consumer. However, we don’t believe this is as valuable as having a varying exposure to overall market beta. Firstly, this is likely to result in significantly more taxes. Second, factors are notoriously hard to time and as AQR’s Cliff Asness puts it: “factor timing is likely even harder than market timing.” Put simply, we don’t believe the value in having Equity Hedge Fund exposure is their ability to weigh relative equity factors, but as a useful tool as part of an overall bucket to weigh relative macro exposures.

We recommend our vol scaled offering. But, doesn’t this change this hedge fund exposure into a single manager product, why not do a fixed scaled exposure? We believe the value in hedge fund exposure is its relative weighing of different asset classes which isn’t necessarily akin to market timing. Hedge Fund’s have demonstrated their ability to obtain high amounts of alpha during large and sustained market drawdowns simply by over weighting other factors during those periods. However, this has largely come at the cost of upside. By targeting a constant level of risk, the return attributes are more significantly more attractive as the alpha during drawdowns is retained, but the ability to capture the upside is greatly improved.

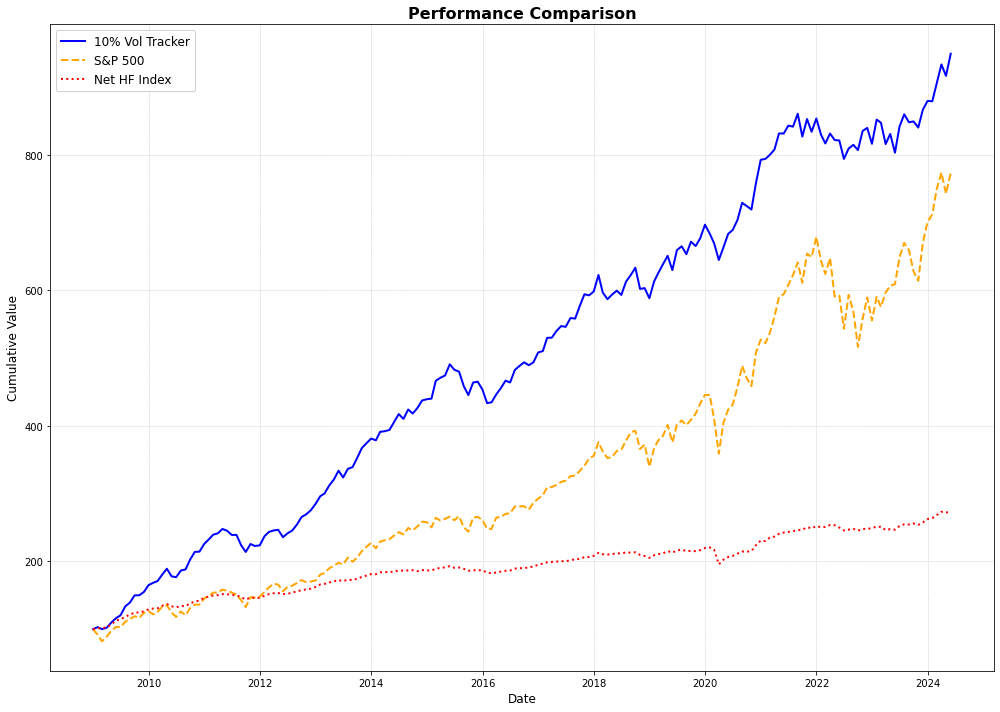

Here is the performance of the vol scaled tracker including transaction costs and modest slippage assumptions:

Clearly, this is an attractive return profile as our Tracker (tax unoptimized version) was able to achieve greater returns with significantly less volatility, less significant major drawdowns (with a tradeoff of slightly more accentuated pullbacks) and a much higher Sharpe ratio than the SP500 during this period.

Here is a snapshot of our actual 10 vol product positioning on 10/22/2024:

As can be seen, a wide variety of strategies among a diversified basket of hedge funds is largely timed exposures to common assets with fees eating into the majority of their attractive attributes, but the combination of our proprietary methods and diversifying hedge fund strategies leads to a return stream that is significantly more appealing than the SP500 itself, even during a prolonged 16 year bull market.

Essentially, these factors are the same as you would find in a risk parity strategy, but the allocations are not informed by risk or single manager insight, but by the collective wisdom of the most sophisticated investment managers in the world.

Can you replace market beta?

Just like how conscious portfolio allocations like risk parity or more tailored approaches like the permanent portfolio, it is recommended to replace such exposure with an efficient Hedge Fund allocation only if one is okay with slight market tracking error.

It isn’t advised to entirely replace a passive portfolio of stocks and bonds as there is uncertainty that could arise from an investment deviating from a benchmark like the SP500 or 60/40. One should not expect to outperform during a bull market, but there is the expectation of outperformance of both total and risk adjusted returns over an entire market cycle.

This approach, however, can entirely replace an investors allocation towards alternatives like various active single manager investments, small cap and international stock exposure, private equity, private credit, hedge funds and investment strategies like risk parity.

In that sense, the hedge fund strategy should be viewed as a complement to a passive market-cap weighted investment at a 50% allocation and a 25% allocation to the beta replacement HF strategy at 10% vol and 25% to our managed futures offering of their total portfolio allocation.

One can obtain even more efficient exposure with stacking the HF strategy and managed futures exposure by allocating only 50% of ones portfolio but obtaining 50% exposure to the HF strategy and 50% to managed futures.

We do not go into as much depth here as our Managed Futures article or Part 1, however contact us to learn more about anything from tax minimization to expectations for performance.