Creating a Better CTA Return Profile with a Fully Top-Down Replication Approach - Part 1

Why the SG CTA Index?

Simply put, we believe managed futures is the best strategy within the alternatives space, with negative average correlation to the SP500 over an entire market cycle and the ability to make large returns during periods usually defined by unexpected inflation or deflation.

Momentum remains the primary component, but carry, mean reversion, and seasonality make up a meaningful portions as well.

The Index itself is equal weighted the top 20 managers within the space. Thus, the Index consistently represents top percentile performance as the cross section of constituent performance is positively skewed.

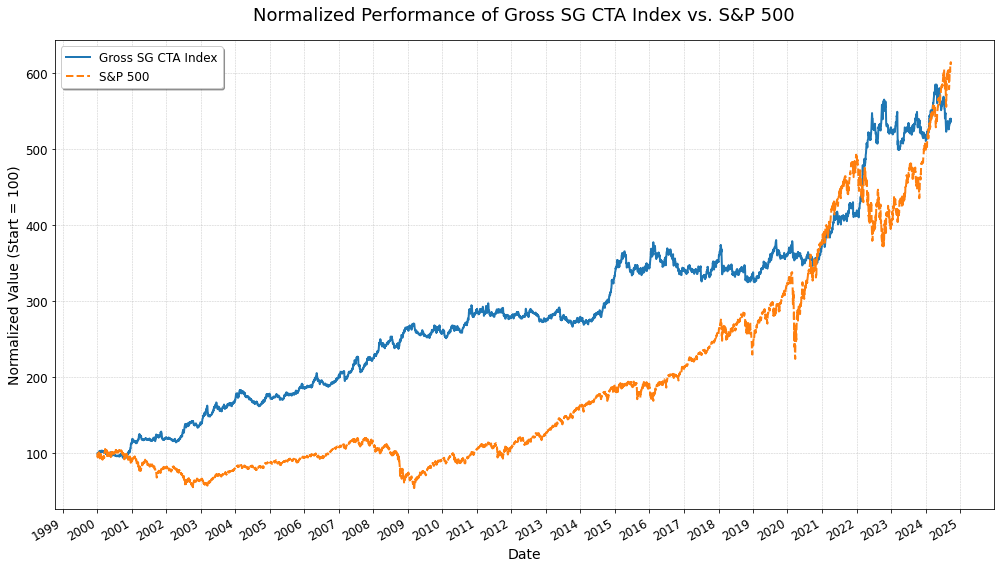

Gross-of-fee SG CTA Index (January 2000 - September 2024):

Here are the results from Dynamic Beta’s 4-factor replication model (SP500, 10-year US Treasuries, Euro, Crude Oil), and then using monthly data to calculate the following metrics (July 2008 - July 2023):

Why Managed Futures Funds are Ripe for Replication - Andrew Beer @ Institutional Investor

The replication was able to achieve a more appealing return profile while having high correlation during periods of time where the Index was performing well and did well at reducing the cost of carry outside those periods. Performance outlined in DBI’s article here: https://www.institutionalinvestor.com/article/2c5hppx3zyokqv8e2vmyo/opinion/why-managed-futures-funds-are-ripe-for-replication.

We of course believe there is room for improvement, although as history has demonstrated, combining the individual approaches of different smart people can lead to the highest expected out of sample performance.

We actually do something we call triple-layered replication, the engine behind our aim to increase risk-adjusted returns beyond the “single-layered” replication approach that we hypothesize is being used by the current industry leaders.

A well designed model will be able to digest new data and balance that information against older data points, but it does not treat them equally. We build on top of that approach, not only for the sake of seeking higher risk-adjusted returns, but to optimize for tax efficiency as well.

Why the SG CTA Index and not the SG Trend Index?

Since inception to 10-25-2024, the gross-of-fee SG CTA Index has a sharpe ratio of roughly 0.81 since inception compared to the 0.66 of the gross-of-fee SG Trend Index. The diversified strategies outside of pure trend have done well at improving the overall return profile.

All else being equal, a higher sharpe ratio is more desirable because it can represent a difference in investor psychology with regards to both uncertainty and risk while holding the investment.

Our Goal

- (Tax Optimized Gross Index Plus)

From a fundamental standpoint, top down replication within Managed Futures is likely the hardest category as turnover is significantly higher than other hedge fund strategy. Static approaches that don’t consider fresh datapoints as distinct from previous ones are unlikely to be good fits out-of-sample. Not considering the skewness of asset classes is also likely to dampen the relative attractive return attributes. The different strategies involve slightly different time frames and holding periods. You also need an adaptive approach in order to capture changes in the underlying strategies and fund constituents and as such we use a form of machine learning to tackle the overarching problem. This makes this particular problem quite complex.

We don’t believe bottom-up approaches are value additive, as these approaches are unlikely to adapt to changes in the underlying Index something similar to what large Investment Banks offered but subsequently failed to deliver out of sample. It is essentially a managed futures strategy that happens to be overfit to track the Index on historical data!

Thus the only current provider in the space for this type of exposure is DBMF.

There are more things to consider, but simply put for our Managed Futures product, we care highly about overall net risk-adjusted performance which is why we use these 5 factors: SP500, 10-year US Treasuries, Euro, Crude Oil and Gold.

Our goal is superior risk adjusted performance to even the gross of fee Index, which represents top percentile total and risk-adjusted performance within the underlying funds.

However, taxes are a drag on performance. There are 2 components to managed futures performance: the excess returns of the strategy and cash.

Let’s walk through the numbers:

- The expected excess return of the Gross SG CTA Index (2000-2024) is around 4.25% vs 2% for the Net Index

- The long term expected short rate is 2.9% (2024 Long-Term Capital Market Assumptions @JP Morgan)

Put simply, futures have the benefit of being taxed 60% long-term and 40% short-term for a blended rate of 26.8%. Most managed futures fund utilize a Cayman structure, where commodity profits are taxed as ordinary income, in this example, 37%. We assume commodities make up approximately 25% of the overall returns. Short term treasury bills are also taxed as ordinary income.

Thus the long run expected return is (4.25% * 75% * (100% - 26.8%)) + (4.25% * 25% * (100% - 37%)) + (2.9% * (100% - 37%)) ≈ 4.8%. In other words, the tax drag is about 1/3 of overall returns.

For an investment in the SG CTA Index, where fees would eat up more than half of the excess returns, this would result in a net return of approximately 2.8% as opposed to 1.8% for cash.

__________________________________________________________________________________________________________

With our approach, from only a tax perspective:

- Cut down on short term rate taxes from 37% to 26.8% or a roughly 33 bps increase

- Increase short term rate by a historical 40-60 bps implicitly through basis arbitrage

- Cut down on capital gains from the realization of commodity futures PnL or a roughly 20 bps increase

- Cut down on capital gains from the realization of non-commodity futures PnL or a roughly 40 bps increase

All of this resulting in a reliable compounded more than 100 bps in “tax alpha” on average annually.

For perspective, this is magnitudes larger than what the active equity segment seeks to generate in excess returns of 50bps over the long run, however this approach in particular is guaranteed. ___________________________________________________________________________________________________________

More markets is better from a single-manager perspective, sometimes

Funds, like managed futures, diversify across many markets because there may be conflicting signals that can result in a more refined overall position on an underlying market driver. Going from 20 to say 50 markets, is likely to increase overall risk adjusted performance because these many markets display slightly different information in regards to the underlying forces.

There is a delicate balance between having too little and too many markets. Generally, you want enough markets to be able to latch onto the underlying drivers of performance during large simultaneous market moves, in a risk efficient manner. Having too many markets can actually be determinantal to the crisis alpha component that managed futures funds seek to provide.

Going from say 50 markets to 100s of markets can provide plenty of challenges to the funds themselves. Many of these markets are illiquid and more likely to have properties that can be quite harmful to the strategies that the funds use to trade. Portfolio construction is not a trivial task and is something that can greatly alter the performance of a managed futures fund: the allocation of risk to the different markets within a portfolio. The underlying strategies are often leveraged 3-5x or even higher, and there are often large market impacts to trading in these illiquid markets.

Lastly, these funds are continuously updating their methodologies. Whether this is adding a new component, such as economic trend, adding new markets, changing strategy parameter adjustments, upgrading risk controls, or implementing a different way of constructing the overall portfolio.

Replication Intuition and Why It Works

The premise of replication is that the 100s of markets that the underlying funds may trade can be represented in the form of a basket of factors. Under the hood, even though there are 100s of markets seemingly providing diversification there are really mostly 1-3 discernible underlying bets at any given time.

Put simply, the long and short positions in the many equity markets ranging from those in emerging to developed markets or more esoteric markets like live cattle or sugar can be represented as a common underlying driver that we can obtain using some combination of other factors. When we put on positions in the markets that we trade, we’re trying to obtain exposure to those same bets that an underlying strategy achieves with 100s of markets.

This implies that managed futures can be distilled down to timed exposure to common beta factors and that this underlying is masked behind diversification both within markets and the different strategies that could be incorporated within an entire system.

One major implication of these additional markets we’ve alluded to earlier is that they have often have much worse return distribution properties. In simple terms, they often suffer from things such as asymmetric drawdowns, whipsaws, and price spikes that can often occur. This is likely the result of trade crowding, illiquidity and market manipulation.

This all ties into the underlying strategy relying on accurately forecasting future correlations and volatilities. Since the strategy is leveraged on the basis of past volatilities and correlations, the spike in correlations and volatilities in markets can be quite detrimental especially if a strategy is positioned in a way that it finds itself on the losing side of the majority of their underlying bets.

However, the strategy also somewhat relies on not accurately forecasting future correlations and volatilities in putting up big numbers. It is these two dynamics that can exploited in a targeted manner via a top down replication approach.

Why these factors?

The 5 markets we’ve chosen are simply the most traded and most liquid in the world in their respective asset classes. Global markets are interconnected with common driving forces, which make possible additions less useful than would seem. Similar results can be obtained by picking any combination within various equity, rates, currencies, and commodities markets which affirms that this approach is quite robust.

Performance attribution is also very clear. For investors who are used to dealing with these markets, there is less of an aversion to familiarity as opposed to the novelty of more seemingly complex “black-box” systems.

Other approaches add additional equity markets like emerging markets or currencies like the yen. We don’t view these exposures as that beneficial given their horrific return properties and unlikeness for having more idiosyncratic drivers that differ from markets we already have. More idiosyncratic markets like natural gas are also left out as the underlying funds likely only have a miniscule position in these markets. They also don’t fit in a tax optimal approach.

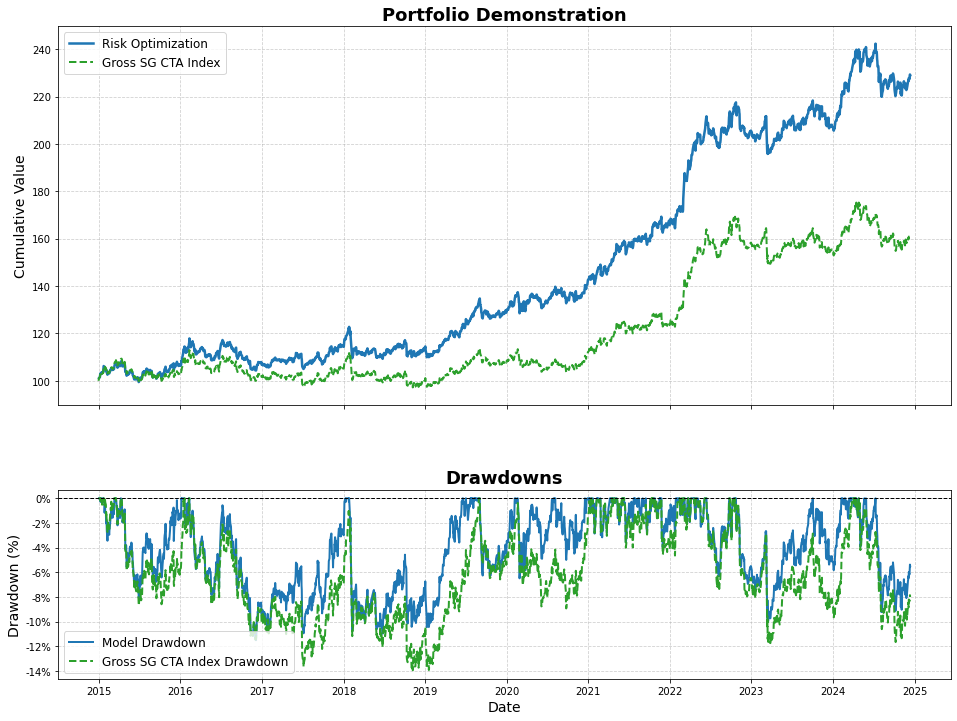

Risk Optimized Gross SG CTA Index

We believe the Index can actually be greatly improved upon.

We work equity factor exposure into the models in order to better manage risk while seeking to maintain the same correlation.

Essentially we seek to provide greater total and risk adjusted performance with the addition of some added downside convexity.

To obtain the below performance, we map out the exposures to our markets through out multi-layered systems and obtain our adjusted equity factor exposure which we then map back onto the original Gross Index scaled by certain factor. In our actual offering the Gross Index would be replaced by our markets exposures.

* The equity factors utilized are part of a group of non-optimized publicly available indices

As can be seen, managing downside risk + adding in some minimal touches without seeking to have much impact on the overall return profile increases the total return while maintaining high correlation to the Index. This approach has allowed for 300-400 bps of excess average annual returns over the last 10 years.

This works as the common driving force behind many of these drawdowns and recoveries is actually very much intertwined with equity beta.

In a more practical application, pre-risk optimization, one can expect a slight haircut in risk adjusted performance as opposed to the gross benchmark. Post-risk optimization, risk adjusted performance is expected to be significantly greater.

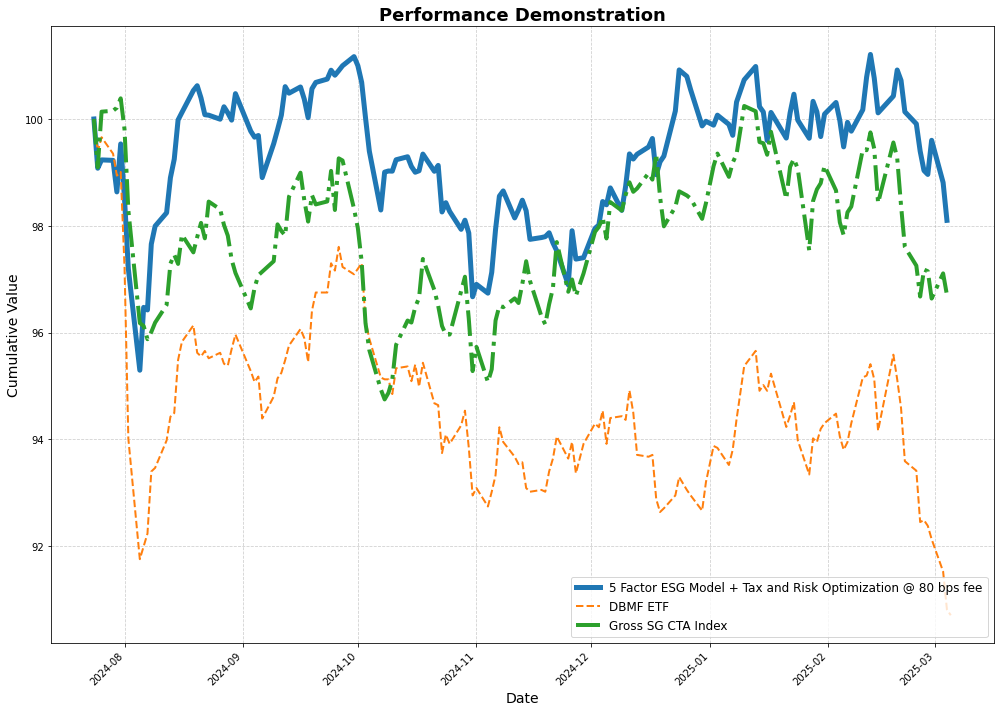

Live Performance

*History has demonstrated that combining the individual approaches of different smart people within the Industry in an equal weighted fashion to often be a superior investment strategy. The expected value of such an investment is much greater than any other weighting scheme given 0 prior knowledge of future performance.

DBMF is currently the gold standard in the space as a fully top down solution.

Again, we view ourselves as an equally-weighted complement to the DBMF etf for this type of exposure. However a taxable investor might consider overweighting or solely investing in this approach given the tax alpha will be hard to overcome.

Here is a chart of our daily total return (started providing live positioning for a client: 7/24/24 - 3/4/2024), ex-post 5 factor model of our risk and tax optimized gross SG CTA Index.

Our approach is specifically designed to limit the types of problems that can lead to this occurrence, which have and will continue to occur. It’s fairly difficult to out perform the Gross Index at all individual points in time, mainly because of it representing a collection of efforts and risk models, but significant outperformance over time is to be expected like pictured above while keeping risk in line with the Index even with a fee expenditure of 80 bps as the additional alpha exposures stacked on top are quite substantial.

This is how allocation to our (net) factors have changed (8/1/24 - 9/1/24). Our rebalancing is non-static and that means we only rebalance if our model implies that the expected tracking error has stepped out of an allowable boundary. This is largely to save on transaction costs without having much at all impact on performance.

As you can see, we don’t always have on positions in all of our markets at any given time. The first layer of models actually consider a wide range of markets beyond the 5 that we list here. The additional layers push down this wide ranging exposure in order to improve the metrics that we care about, along with the exposure work better with our additional risk optimization.

Our additional model layers suggest that it isn’t appealing to maintain positions in any of the markets that we deem unattractive from a higher order metric perspective. In the later part of August, we effectively only have 2 different market exposures: equities and gold.

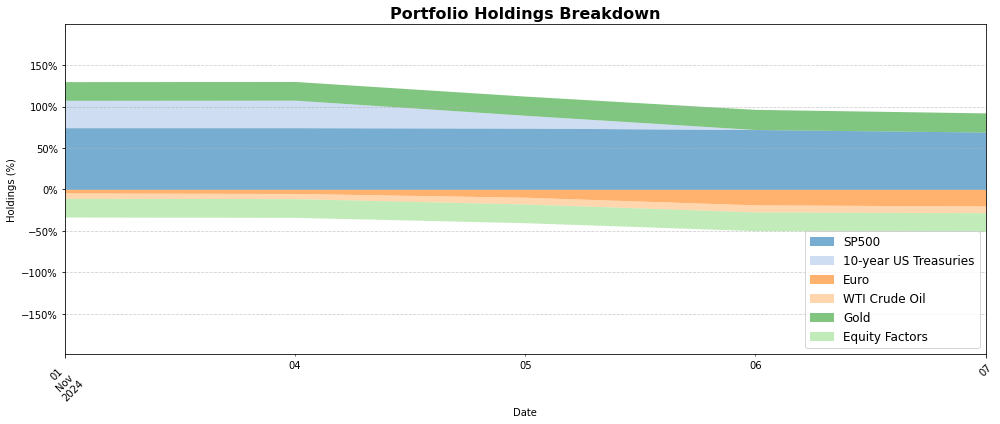

Here is how that positioning has evolved come the first week of November 2024:

* The equity factors utilized are part of a group of non-optimized publicly available indices

The equity factor influences the model and this approach is also mainly made viable due to our approach of only having equity beta representing as the S&P 500.

There is a downside with this approach, particularly if our anti-factors fall less than the market, a low likelihood occurrence that hasn’t ever occurred. The overall benefits still vastly outweigh the potential downsides even if it somewhere where to occur!

The Industry’s Long-Standing Quest for ESG Compliance

Being ESG compliant has been one of the long standing issues in the space amidst the large and growing space in Europe, APAC, and the inevitable growing scene in the US.

There’s a fundamental reason why existing CTAs have not done away with commodities in their approach to managed futures: it degrades risk adjusted and total performance in such a way that long term performance is clearly impacted. This is a issue with there being huge demand, but an insufficient way of actually addressing this cornerstone of the market.

The ultimate goal would be to have a ESG compliant managed futures strategy while retaining the risk adjusted performance of the strategy, or in this case the underlying gross benchmark. There simply hasn’t been a viable competitive approach.

Here is our the changes we made to our original approach:

The folks at AQR suggest the optimal “no-touch” policy for commodities (this guarantees that the investor does not have a harmful macro influence) in regards to meeting any sort of ESG objective: Sustainable Commodities Investing. Nearly all commodities have negative scores in relation to social and environmental factors: labor, access to food and energy, climate change, biodiversity, water, waste and the circular economy. Trading any sort of commodity is likely to have a macro impact on any of these dynamics listed here.

To achieve this previously considered impractical goal, we simply exchange Gold for the Australian Dollar and Crude Oil for the Canadian Dollar in our additional model layers while keeping everything else almost the same. The Norwegian Krone is also a good candidate as a replacement for Crude Oil.

Because of our approach, the additional alpha sources that result from our carefully selected market exposures, portfolio positioning and arbitrage alpha within the product more than makes up for any of the deficiencies that are caused by being commodity constrained.

There is an estimated 100 bps return deduction with the naive replication approach, where this becomes less than ideal. Our approach, however, is still expected to at least meet with the goal of outperforming the gross index benchmark even with a 80 bps management fee and a more attractive post-tax return to boot.

Non-commodity futures also have the benefit of having a significantly more appealing tax profile.

Additionally a benefit of incorporating these equity factors are they implicitly create an overweight towards ESG within the overall portfolio. Again, the incorporation of individual equities is an input within the layered model system so that the resulting performance will remain highly correlated to the Gross Index.

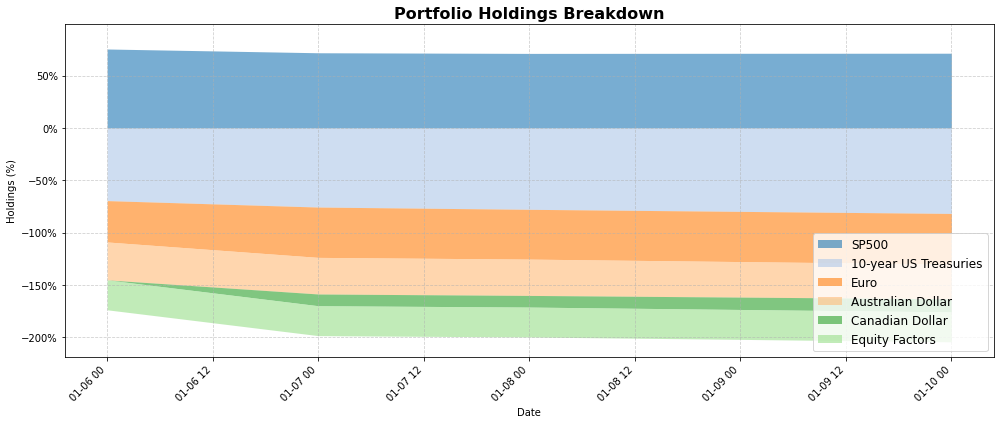

Here is the positioning over the first full week of January 2025:

S&P 500 long exposure can be replaced by something like an S&P Paris Aligned & Climate Transition Index (to meet article 9 or other ESG requirements) without much difference relating to long term performance. You can do a relative value trade where you long an ESG Index in full and short the S&P 500 to match the required broad based equity exposure. * This is only feasible the way we do it due to a variety of reasons

The short equity factor exposure is already creating a more esg-aligned total portfolio, although this is definitely something that can tweaked even more if needed. However, it should already be able to meet article 9 without needing to do so. A ton of additional possibilities.

It’s also much more feasible to implement ESG Indices within this approach compared to a long only equity product or even the vast array of other hedge fund categories. This is simply due to the fact that tracking error in equities is a bug, but here it’s already expected (with a clear benchmark as the icing on the cake).